How Do Credit Repair Companies Work?

Disclaimer: We offer completely free content to our users. However, articles or reviews may contain affiliate links and we may earn a commission. Learn more about how we make money.

Are you considering whether to sign up for paid credit repair services or not? If you have a company in mind, you may have checked their pricing and discovered that it costs about $80 to $120 per month. This may lead you to ask, does credit repair work? And if the answer is yes, then what items can it remove?

Professional credit repair companies can’t work miracles and deliver a new slate. They fix credit reports by challenging errors only. Many services are reputable, but it’s important to know the tell-tale signs of a scammy service.

What is Credit Repair Definition?

Credit repair entails checking reports for errors and asking CRAs to investigate them. Customers can mail letters or file disputes online. During re-investigations, CRAs contact the information furnishers such as creditors or collectors. They ask them to verify the accuracy of the disputed entry.

Repairing your credit may take two forms. The first is a do-it-yourself process. It doesn’t take a brainiac to file a dispute or find errors in reports. CRAs strive to make reports easy to understand by highlighting negative entries. Common mistakes may include late payment errors, wrong account status, or strange accounts. Challenges have a better chance of success if customers provide evidence.

So, what do credit repair companies do if customers can do everything themselves? Consider this, mowing a lawn is the simplest of tasks. But homeowners may not have the time or motivation to do it. They find it easier to hire someone to delegate the task.

A credit repair company brings convenience to the process. Note that the services don’t have any special agreements with credit bureaus. They cannot influence investigations beyond providing evidence passed on by the customer.

There are no free credit repair services. Even nonprofits that offer credit counseling are not fully free. Customers only receive the first consultation at no cost. If they need further help managing debt, they must sign up for monthly services.

How Does Paid Credit Repair Work?

Working with a legitimate credit repair company will be a smooth process. The service may entail the following steps:

Step 1: Receive the initial consultation

Free consultation is not necessary, but it’s advisable. It may be a 10-minute call where the rep explains their services. Large companies perform an automated report analysis. They pull reports from the three bureaus and use automated systems to identify potential disputes. If the firm is smaller, it may offer an expert-led analysis.

Requesting a free consultation from The Credit People

Step 2: Order completion

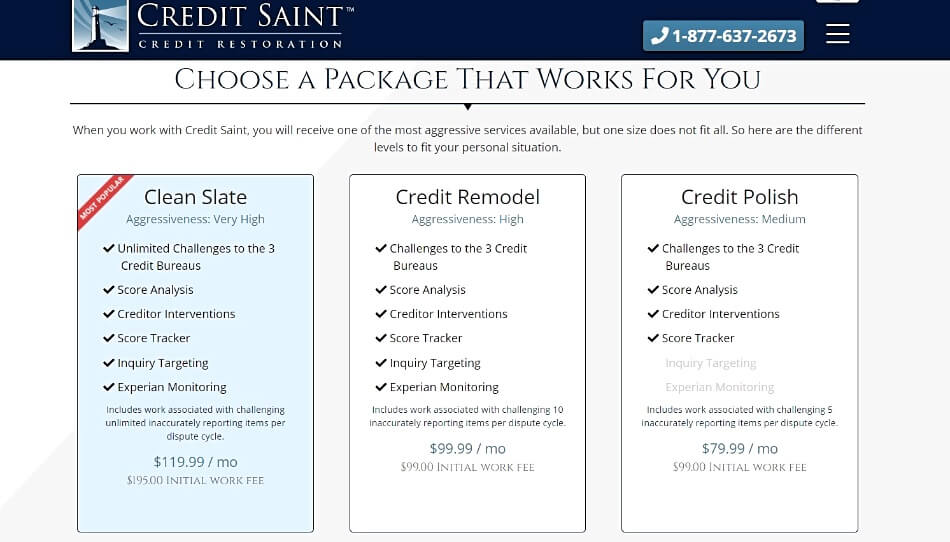

Many repair firms have 2 to 3 packages. Don’t always assume that the best package is the most expensive option. For instance, a service may try to up-sell customers by offering Debt Validation or Goodwill letters. You may never need these services.

Similarly, the most expensive option often includes unlimited challenges. However, the repair firms may advise customers to restrict challenges to only five during each billing cycle. Some services may automatically recommend the best package based on the number of dispute items.

During the order stage, expect to receive a request to add a payment method. The Credit Repair Organizations Act prohibits CROs from charging upfront fees. It also provides a cooling period of three days, where customers may cancel without any penalty.

Step 3: Signing the service agreement

During the sign-up process, don’t overlook the terms of the service agreement. The most important sections include:

- Length of contract – Most services will offer a six-month contract. It does not mean that you cannot cancel earlier.

- Disclosures – The section includes important disclosures as per the provisions of the CROA. It basically states that customers may file disputes with the CRAs directly.

- Service fees – Confirm the initial and monthly fees and when they are due.

- Cancellation options – Customers often find it hard to cancel these contracts. For instance, some firms ask customers to mail or deliver a signed copy of the cancellation. So, confirm the cancellation methods offered by the firm. Ideally, they should make this effortless.

Step 4: Welcome call

Most firms call customers after they have completed their order. The person reaching out may be the assigned case manager. Take this opportunity to ask more questions about the service.

Step 5: Ordering copies of reports

If the service has not ordered reports, they will order them at this stage. An expert should be on hand to review each negative item. Afterward, they should create a custom plan to challenge the potential dispute items.

Step 6: Sending the first set of challenges

Sending challenges is the core service offered by repair firms. They will not send disputes on the same day customers sign-up. Work usually begins after three business days to allow for the cool-off. Some firms offer fast-tracking such as Ovation Credit, but at an extra fee.

Step 7: Waiting for updates

Many customers question if credit repair companies really work. Well, their work ends after preparing disputes and sending them.

Don’t expect to see results or changes within a few days even if the service is monthly. The Fair Credit Reporting Act allows 30 days for standard re-investigations. CRAs may extend the period by 15 days if creditors are taking too long to respond.

At times, the process is quick if there are no hiccups. TransUnion notes that most of their investigations are complete within 15 days. For successful re-investigations, CRAs will issue updated reports within five days. Please allow up to 15 days for delivery.

Step 8: Preparing and submitting any correspondence

Repair firms ask customers to keep an eye out for correspondence from the major credit bureaus. Their letters often arrive in unmarked white envelopes. So, don’t mistake them for junk mail. The CRA may be requesting additional documents to support a case.

How Much Does Credit Repair Cost?

Well, customers pay two kinds of fees with paid credit repair services. The first fee is the initial setup. It’s deducted in 5 to 15 days. The amount caters to the cost of:

- obtaining credit reports from third-party partners;

- identifying potential dispute candidates;

- creating custom plans;

- preparing the first round of challenges.

During DIY credit repair, consumers can receive free reports through annualcreditreport.com.

Monthly rates range from $69 to $150 with some companies offering single-package pricing. Expensive packages often contain plenty of extras, like ID protection, creditor interventions, and score updates. Here is a sample of charges from the top five firms:

| Company | Setup Fee | Monthly pricing |

| Lexington Law | $89 — $129 | $89.85 — $129.95 |

| Credit Saint | $99 — $195 | $79.99 — $119.99 |

| CreditRepair.com | $69.95 — $119.95 | $69.95 — $119.95 |

| Sky Blue | $79 | $79 |

| The Credit Pros | $119 to $149 | $69 to $149 |

A few firms and professionals charge for each item removed from your credit report. What is the acceptable amount to pay for professional services? Generally, paying more than $130 for credit repair services is too much.

Be aware of other charges. For instance, firms will ask customers to set up automatic payments or allow credit drafts. On the renewal date, they will attempt to charge the card or bank account. If the payment fails, there may be a penalty. For instance, Lexington Law states that they charge a late fee of $19.95.

Repair firms bill for services rendered at the end of the month. If the customer cancels before the renewal date, they may receive a partial bill. Not all firms do this. For instance, The Credit People allows customers to cancel anytime without any charge.

How Long Does Credit Repair Take?

Fixing your credit depends on the number of errors. That’s because experts recommend filing not more than five disputes at a time. The Fair Credit Reporting Act gives CRAs the power to label challenges as “Frivolous.” Experts claim that they may do this if the customer is sending too many disputes. So, if the client has 10 potential disputes and sends about three disputes per month, it may take up to three months to finish the process.

CRAs may respond to disputes by asking for more information. It may contribute to delays. Challenges also fail, leading firms to file for redisputes.

Customers stay with credit repair companies for an average of six months. Some firms will recommend the best time to cancel the service. An online dashboard may also have a progress tracker indicating the best time to cancel.

When Should You Hire a Credit Repair Company?

Paid repair services are still worth it because of the following reasons:

1. Time savings

Spotting errors and filing disputes all require a bit of time. Repair professionals handle everything, freeing up customers to focus on other matters.

2. Easy to get started

People put off credit repair because they are too busy. Hiring a repair firm is a no-brainer. We’ve made it easier by reviewing top credit repair companies like Sky Blue, Credit Saint, and Creditrepair.com.

3. Personalized guidance

Many firms are committed to offering help beyond credit reports. They assign case advisors to customers who offer expert advice in other areas.

4. Score, disputes, and report tracking

During the repair process, customers receive updates on the status of cases. The firms also partner with other companies to provide regular reports and updated credit scores. Firms such as Creditrepair.com and Ovation Credit offer ID protection on some packages.

5. Extra features

A reputable service will also provide a host of other value-added services to help improve your credit, including:

- Sending debt validation letters to debt collectors, asking them to verify the legitimacy of debt accounts;

- Offering other ways to repair poor credit such as recommending the best credit rebuilding products;

- Appealing to creditors to remove negative information voluntarily by writing GoodWill Letters;

- Drafting cease & desist letters to instruct collectors to cut off communications;

- Putting a good word by sending lender or employer recommendation letters.

How to Avoid Credit Repair Scams?

Paid repair services are often dismissed as unnecessary and scammy. However, this is not the case. Many customers have found it easier to work with legit credit repair firms.

Various warning signs can point to a scammy service. Most often, rogue operators will be going against the provisions of the Credit Repair Organizations Act. Just use the following tips to stay safe:

- Choose companies that are highly reviewed;

- Never subscribe to a service that promises to challenge accurate entries;

- Avoid and report services that charge an advanced payment before sending challenges;

- Avoid providers using illegal credit repair techniques such as credit sweeping or jamming;

- Don’t sign up for a service that promises to assign a new Employee Identification Number;

- Watch out for other telltale signs on the service website;

- Ensure a service is not making tall claims such as rapid score improvements.

Customers may choose companies that offer service guarantees. If there are no results, they issue refunds.

Bottom Line: Do Credit Repair Agencies Work?

Yes, they do work, and there are certain advantages of working with professional credit repair experts. They handle all aspects of the process, from dispute identification to filling challenges. Most services make it easy to track progress, report, and score challenges. Still, it’s possible to repair credit without any intervention and achieve professional results.