How to Fix Your Credit?

Disclaimer: We offer completely free content to our users. However, articles or reviews may contain affiliate links and we may earn a commission. Learn more about how we make money.

The term “fix my credit” implies identifying errors in reports and trying to remove them. What’s more, it’s possible to request lenders to remove accurate entries from reports. The latter option works with recent late payments.

Credit repair services are hugely popular with consumers. They help them challenge and remove certain negative items from their reports. They can’t guarantee more success than DIY credit repair. But they are more experienced. For instance, Lexington Law, a top provider of repair services, has handled over 221 million disputes since 2004. They have about 500,000 active customers at any given time.

But here is the deal. It’s possible to execute credit repairs without any outside assistance. We’ll outline the entire process and resources. But why are credit repair companies still popular? Keep reading to find out:

8 Steps to Fix Your Credit Score

Free credit repair can happen on its own. How? Well, past credit mistakes don’t remain on reports indefinitely. Negative entries reach a certain age and fall off the reports. For instance, late payments only remain for seven years. Their impact on scores keeps diminishing as they age.

Active accounts in good standing may stay on reports indefinitely. That’s because you can keep using a card for many years as long as it’s active. Closed and fully paid accounts have a shelf-life of 10 years.

Removing accurate items without the intervention of a lender is difficult. But these step-by-step credit repair tips can help challenge inaccurate information:

Step 1: Get free credit reports

How do reports work? Think of them as files containing details on current and past credit accounts.

Apart from Equifax, Experian, and TransUnion, there are lesser-known consumer credit bureaus. For instance, payday lenders report payments to Clarity. But the three CRBs supply reports for mainstream lending decisions and score calculation.

Lenders are at liberty to select where to report consumer information. So, reports may have different details. It also means that one report may have errors while another may be error-free.

Some CRBs permit users to add alternative credit data such as bill payments. The information is also susceptible to errors

4 places to order free report copies

1. Annualcreditreport.com

Jointly operated by the three CRBs, the site came into existence following the passing of the Fair and Accurate Credit Transactions Act that entitles consumers to one free report annually.

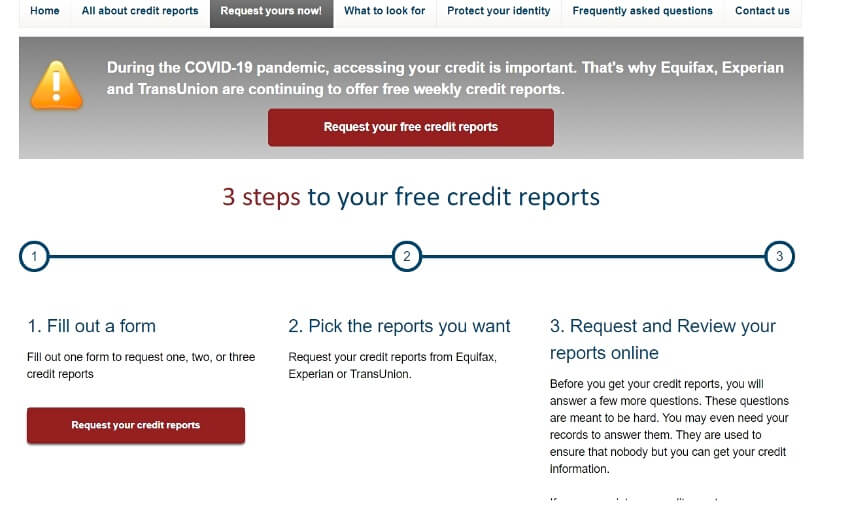

The CRBs have committed to offering free weekly credit reports until April 20, 2022. It's their contribution to easing the hardships brought about by the COVID-19 crisis.

Start by creating an account here. Complete the verification, and receive the reports instantly. The site also mails report copies but this may take 15 days.

AnnualCreditReport.com website

2. Create an account with each CRB

CRBs also offer free reports online. Equifax first requires customers to sign up for a free Equifax account. Experian provides reports through their dashboard. They also offer many free features, including debt summary, score analysis, and monitoring. For free reports, TransUnion will redirect you to annualcreditreport.com.

3. Credit monitoring websites and finance apps

Several credit monitoring and finance apps offer free credit reports to first-time users. But customers will need to pay a monthly or yearly fee for ongoing credit report updates. Popular websites for free reports include CreditKarma or myFico.

4. Credit repair organizations

Thinking of signing up for a credit repair service? As part of the initial work, the services retrieve credit report copies for free. After the service commences, customers also receive regular report updates.

Step 2: Check for questionable entries and erroneous information

Most reports have errors. Why is this the case even with the digitization of credit management and reporting? Errors typically happen because of:

- People applying for credit under different names;

- Lender submitting incomplete information to CRBs;

- Mistakes when transferring details from hand-written credit applications;

- Entering the wrong SSN number;

- Lenders applying payments to wrong accounts.

Knowing the categories of credit information makes it easier to spot errors. The key sections in credit reports include:

1) Personal identifiable information (PII)

CRBs use this information to match details to correct credit reports. PII details include Name, SSN, addresses (present and past), telephone numbers, and employers. Mistakes typically arise with listed addresses and names.

2) Account records

The section includes the particulars of active and closed accounts, including:

- Date opened;

- Account and loan type;

- Balance and available credit;

- Credit limit;

- Monthly payment amount;

- Date of last payment;

- Repayment frequency;

- Current status (Paid as agreed, Closed never late, settled account, or past due).

Confirm that all account entries are accurate. Most mistakes revolve around wrong account balances or limits. Such mistakes can increase the credit utilization rate.

Pay particular attention to the current status. For instance, a mistake may cause a fully paid account to appear as settled in full. Settled accounts may decrease scores by up to 100 points. The status implies that the borrower has paid less money than owed.

Duplicate accounts are also rampant, particularly for people with collections accounts. That’s because the accounts may change hands several times. Two companies may inevitably report on the same consumer.

3) Public records

The public record information contains details about bankruptcies or collections accounts. Bankruptcy is pretty much self-explanatory. Collection accounts arise after the creditor charges off the account. It happens when the borrower defaults for 6 months to 12 months.

4) Inquiries

An inquiry is a request to the CRB to furnish the report. There are soft and hard inquiries. Lenders conduct soft inquiries to pre-qualify borrowers and send loan offers. Personally ordering report copies also qualifies as a soft inquiry. “Soft” means that they have no effect on scores, and there is no need to dispute them.

Borrowers must authorize a lender to conduct a hard pull during the lending process. Scoring models treat hard pulls or inquiries as negative entries. Can they be disputed? Yes, but once hard inquiries age for over 90 days, their impact reduces. They also fall off reports in two years.

But don’t ignore inaccurate hard inquiries. Some lenders review reports to see the number of recent hard pulls. They consider if the credit evaluations resulted in new accounts. If other companies are denying credit to a customer for some reason, a potential lender may be less inclined to advance credit.

Step 3: Reach out to creditors and open a dispute with the bureau

Should I contact the lender first and wait for them to make corrections on their end? Well, the best advice is to contact both parties.

Use available channels to reach out to the creditor. For instance, check their site for support numbers, email support, or live chat. They may resolve the issue quickly since they have credit account details. But have your credit reports on hand and any supporting evidence to make your case clearer?

How can I contact the credit bureaus?

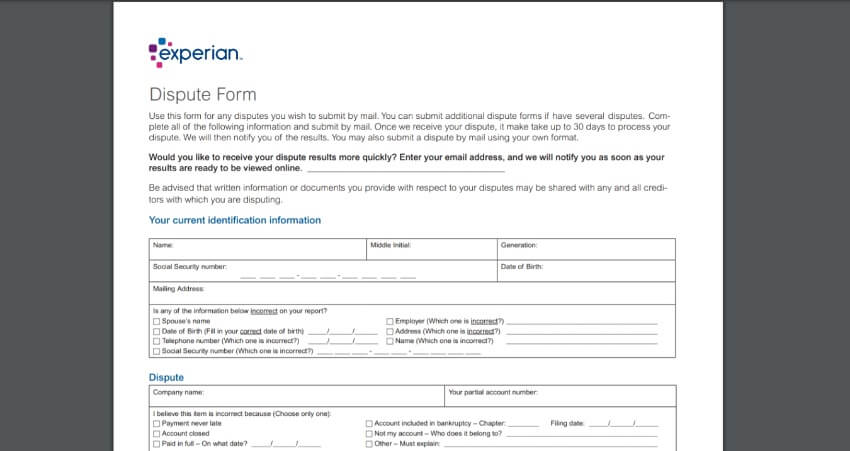

Most sources recommend writing a 609 dispute letter. But it’s not always necessary. Experian even advises against purchasing a 609 dispute letter. They provide a dispute form that customers can download, fill and send by mail or upload online. The service also provides a full online dispute process. Use these resources when disputing errors with Experian:

- Instructions to dispute by mail;

- How to upload the scanned dispute form;

- Online dispute center guidelines.

Example of Dispute Form Experian

Equifax also makes it easier for customers to send disputes. They provide the following resources:

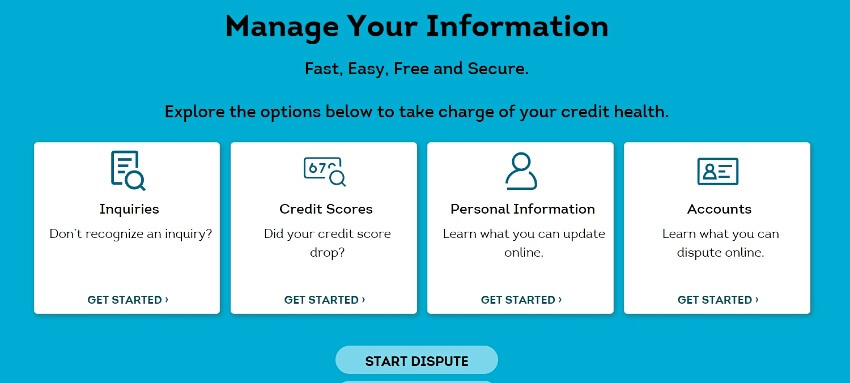

TransUnion welcomes disputes from customers. They also have a comprehensive FAQ section, addressing common dispute questions. They provide the following resources:

Online disputes are faster as they are not subject to delays from the mailing process.

TransUnion Start Dispute & Get Status

What actions do CRBs take after receiving disputes?

They contact the information furnisher, for instance, a creditor or public record resource. The CRB requires confirmation that the entries are accurate. If a lender finds errors, they must recommend the appropriate changes.

How long do investigations take? Most CRBs give a timeline of 30 days. TransUnion revealed that many investigations concluded within two weeks.

After implementing corrections, the bureau may issue an updated report. If the error resulted in credit denials, borrowers can request bureaus to send their updated reports to past lenders.

Step 4: File redisputes

At times, legitimate challenges fail. Some creditors deal with many dispute results and may not investigate claims substantially. Deleted items may even reappear. Furthermore, some creditors go out of business making it challenging to verify entries.

Don’t fret. CRBs allow customers to challenge the same entry several times. For instance, Transunion advises customers to submit supporting evidence to reopen investigations. Examples of commonly requested evidence include:

- Canceled cheques;

- Account statements confirming status;

- Money orders;

- IRS notices or letters;

- And more.

Veterans may dispute entries resulting from medical debt covered by the VA. For instance, Equifax only requires a “VA notification letter” or extra documentation.

Step 5: Handle overdue and collection accounts

As part of improving your credit scores, make a plan to deal with overdue and collection accounts. Do you owe a lot? Well, weigh if it’s better to spend money on credit repair services or paying down debt.

But what should be paid first?

For overdue accounts late for 30-day to 180 days, consider raising enough funds to cater to the monthly payments. Keep the account from being charged off.

Collections and bankruptcies are more severe than other types of negative marks. What if an account is already in collections, does paying it off remove it from reports?

No, the collection account remains on the report. Unpaid or paid collection entries have similar effects on scores. That’s why it’s better to prioritize active debt accounts over collections accounts. Lenders may remove late payments voluntarily after paying down outstanding balances.

Step 6: Writing Goodwill adjustment letters

Have you recently run into financial trouble that made making payments difficult? Looking for a way to have the negative entries removed? Consider writing a Goodwill letter. It’s a request for the lender to voluntarily clear credit history mistakes.

But don’t count on this technique working. CRBs ask lenders to uphold high accuracy standards and discourage the removal of accurate entries. Some companies have compassionate policies and will agree to remove the negative entries. On request, many credit repair agencies can also send Goodwill letters to creditors.

Step 7: Pay for delete

Pay for delete mostly involves petitioning debt collectors to remove prior negative entries. In return, you offer to pay the outstanding loan amount or credit card balance. Pay for delete letters may come in handy when dealing with collection agencies. But again there are no assurances of them working.

Step 8: Add consumer statement to reports

After exhausting all possible ways to repair your credit, consider adding consumer statements. It involves adding a personal statement to explain a negative entry. Most CRBs allow up to 100 words per statement.

It explains the reasons for the negative mark, for instance, “I was not able to honor the loan repayments after closing my restaurant following covid-19 shutdowns.”

While it’s not a cure, it may influence a potential lending decision or rental approval.

Benefits of Credit Repair Companies

Many sources are quick to tell people that they don’t need credit repair services. Should you believe them? We regularly review legit credit repair companies. Speaking from their point of view, there are several reasons why their services are invaluable:

1. Free credit consultations

The services use initial consultations to get customers through the door. But it’s possible to take full advantage of the free credit help.

For instance, after filling out their form, The Credit People assigns someone to contact you. The credit expert explains what to expect from their service. It’s a chance to get invaluable pointers about potential dispute candidates.

Creditrepair.com goes above and beyond. They also provide free credit improvement plans, negative item reviews, and score summaries.

Creditrepair.com Free Evaluation Offer

2. The professional argument

Many sources may show you how to fix your credit. But it may be difficult to beat the value offered by credit professionals. It’s the same argument for hiring a plumber to install a new sink. Sure, the tutorials are within easy reach but a plumber may make the process seem effortless. They are also less likely to make simple mistakes.

Not all customers have a problem-free experience when challenging errors. In repair reviews, we find customers who turn to repair services to deal with specific situations.

3. They can spot opportunities

Loopholes do exist in the credit reporting and repair process. For instance, some sources report that debt collectors may be slow in responding to verification requests. They may even ignore them. If the 30-day window for verifying entries ends, the CRBs have to remove the entries.

Credit experts may be good at spotting such procedural loopholes. But don’t always count on this happening. Most credit repair organizations only go after inaccurate information. But at times customers get lucky.

4. Help to fix bad credit

Due to stiff competition, repair agencies attempt to offer plenty of add-ons. The Credit Pros, for instance, assigns Certified FICO© professionals to each customer. The pros offer free credit rebuilding guidance to improve your credit scores.

5. Save time

Saving time is key. But don’t rush to sign up for credit repair. It’s not worthwhile to pay for credit repair when there are only minimal negative entries to challenge. Conduct an independent analysis before exploring these services.

However, some honest vendors first assess your reports for negative entries. Afterward, they recommend their services.

Cons of Using Credit Repair Services

One of the best ways to repair credit is by seeking professional help. But these services also have limitations:

1. Mismatch of expectations

If a credit repair company is charging $79 per month, it’s typical to have high expectations. Should a professional not achieve faster results?

Whether it’s a company or individual filing disputes, the investigation process doesn’t differ. At times, CRBs respond to challenges after 45 days. Most repair companies inform customers to expect changes in the first 60 days.

2. No assurance of results

Repair companies cannot predict how bureaus and creditors react to challenges. Some companies don’t offer refunds or guarantees. But there are exceptions.

Some of the best firms have no qualms about offering service guarantees. For instance, if Credit Saint can’t clean credit reports in 90 days, they can issue a refund.

3. Most companies charge monthly fees, not per-deletion fees

In the past, some companies charged per item they successfully removed. Now, many charge monthly fees.

4. Prevalence of scammy services

Some unscrupulous services have given legitimate companies a bad rep. But there are ways to stay safe. Be wary of services that claim to fix credit fast or demand upfront monthly payments.

Extra tips to build up credit

Looking for tips to recover from a disastrous credit situation? You can read our article about how long does it take to fix your credit. But the following is a summary of some of the tips discussed there:

- Applying for secured credit cards or loans. The products don’t work exactly as traditional loan products. Lenders will require a security deposit before advancing the loan. But they are great for adding positive credit history to reports.

- Becoming an authorized user. Card companies permit primary account holders to add secondary users or authorized users. Listed persons receive the same history when it’s reported. Consider approaching someone with stellar credit. But there is no need to charge their card.

- Keep credit utilization rates low. Maintain a utilization rate of 30% or lower on revolving credit accounts. Consider paying down balances or asking creditors to increase the credit limit.

- Pay down credit card debt. When dealing with high debt, make payments to accounts with high interest rates.

Bottom Line

We have examined the step-by-step process of fixing credit. It entails error identification, dispute filing, and redispute filing. CRBs have come a long way to addressing disputes. Previously, verifying errors was a frustrating experience with long wait times. Now, all the CRBs are showing a willingness to help. They are providing dispute forms, helpful information, and access to online dispute centers.