What Credit Score is Needed to Buy a Car?

Disclaimer: We offer completely free content to our users. However, articles or reviews may contain affiliate links and we may earn a commission. Learn more about how we make money.

As of April 2021, the average transaction price for a light vehicle in the US was estimated at $40,768. In the 90s, new cars only set consumers back by about $15,000. Vehicles are certainly becoming more expensive, and with 85% of new car purchases being financed, it’s natural to wonder what is a good credit score to buy a car.

The average APR for car loans was at 4.31% for Q4 2020 as reported by Experian Information Solutions. It’s not an exact science to use this rate to determine how much a loan may cost. That’s because rates differ by the consumer’s creditworthiness. Prime consumers — people regarded as having good scores — pay auto loan rates of about 3.69%.

We’ll look at score ratings and corresponding loan rates for both used and new cars. We also dive further into steps to take when purchasing vehicles with bad credit. You’ll gain strategies to increase credit scores to buy a car and avoid expensive repayments.

What is the Minimum Credit Score Needed to Buy a Car?

Individual loan originators determine the lowest score they are willing to accept before approving new customers. Banks, which are the biggest lenders, only go for prime consumers (660 to 719 range).

Captive auto lenders — companies set up to offer loans for a particular dealership or automaker — may accept borrowers with ratings as low as 620.

Outside the normal pool of traditional financial corporations, there are private and smaller lenders. The credit score needed to buy a car with some private lenders may actually be Zero! That’s because they prioritized getting paid rather than checking scores. So, their approach is to look at the customer’s ability to pay rather than their past financial mistakes.

Private lenders can operate this way as cars are assets that can be repossessed in case borrowers become delinquent. Now, this does not mean that consumers should blindly trust them.

And what credit score is needed to buy a car for students? Lenders that specialize in student car loans generally check for good credit scores, which means 660+. They also consider sources of income and some go as far as checking the GPA if the student’s income cannot be properly substantiated.

Car Loan Rates By Credit Score

The following table reveals the expected average car loan interest rate by credit score from data contained in Experian’s automotive industry insights for Q4 2020. It’s tabulated for new car loans. (Check the next table for used cars).

| Tier | Loan Rate | Loan-term | Amount Financed |

| Super Prime (781 to 850 ) | 2.65% | 64.69 | $32,298 |

| Prime (661 to 780) | 3.69% | 71.18 | $37,189 |

| Near-prime (601 to 660 ) | 6.64% | 74.03 | $36,951 |

| Subprime (501 to 600 ) | 10.58% | 73.30 | $32,230 |

| Deep subprime (300 to 500) | 14.20% | 72.04 | $27,342 |

The following table presents statistics for used car loan rates by credit score:

| Tier | Loan Rate | Loan-term | Amount Financed |

| Super Prime (781 to 850 ) | 3.80% | 63.07 | $23,304 |

| Prime (661 to 780) | 5.59% | 66.66 | $23,890 |

| Near-prime (601 to 660 ) | 10.13% | 66.90 | $22,484 |

| Subprime (501 to 600 ) | 16.56% | 64.25 | $18,768 |

| Deep subprime (300 to 500) | 20.30% | 60.26 | $16,014 |

Insights:

Based on the following numbers, one thing that jumps out is how the average APR for a car loan varies depending on whether a car is used or new. For the period, the average prime borrower would have paid a rate of about 5.59% for a used vehicle compared to 3.69% for a new automobile.

The auto loan rates by credit score further reveal that loans become cheaper the higher the credit tier a person climbs. For instance, if a super-prime consumer qualified for a $40,000 car loan for a term of 72 months at a rate of 2.65%, the total interest would be $3,308. The car would end up costing $43,308.

If a near-prime consumer took out the same credit product, they would expectedly pay $8,605 in interest charges, bringing their overall costs to $48,605 — based on the average APR for a car at 6.64%.

It’s clear across the board that the best credit score to buy a car is the highest score. While reaching the upper echelons of credit ratings seems difficult, consider that in Q4 2020, the average credit score to buy a car was 733.

People who opted for used car loans had an average score rating of 671. Both segments of consumers had an increase in scores over the last five years. Scores also increased for the general population in 2020, as reported by CNBC.

Note that some loan originators are expensive even to people with great creditworthiness. A good APR for car loans should fall within the stated loan rates. The APRs may change in the future, depending on the market.

How to Get a Car Loan with Bad Credit?

Auto lenders don’t automatically disqualify applicants because they fall into the near-prime, subprime, or deep subprime categories. Buying a car with bad credit is as viable as buying a car with good credit.

There are potential hazards to look out for and safeguards to implement to ensure that exploitative lenders don’t get their way. Here are some of the best recommendations:

Determine affordability before heading out to lots or dealerships

Never head out to the dealership blindly. Snap decisions are prone to many mistakes. It’s entirely possible to drive back home with a $20,000 car when your income affords you a $10,000 vehicle. Salespeople also try to upsell customers on the latest models and features. “What should I do?”

Step 1: Create a budget that outlines any fixed expenses like rent repayments and variable expenses such as food or gas.

Step 2: Determine how much money is left over to cater for monthly vehicle repayments; for instance, it may be $500.

Step 3: Order FICO credit scores for free from Discover Credit Scorecard or Experian Boost.

If it’s a bad credit score to get a car, confirm the applicable APR based on the APRs stated in the tables above. For instance, if your score is 600, the estimated rate may be 10.58% for new automobile loans.

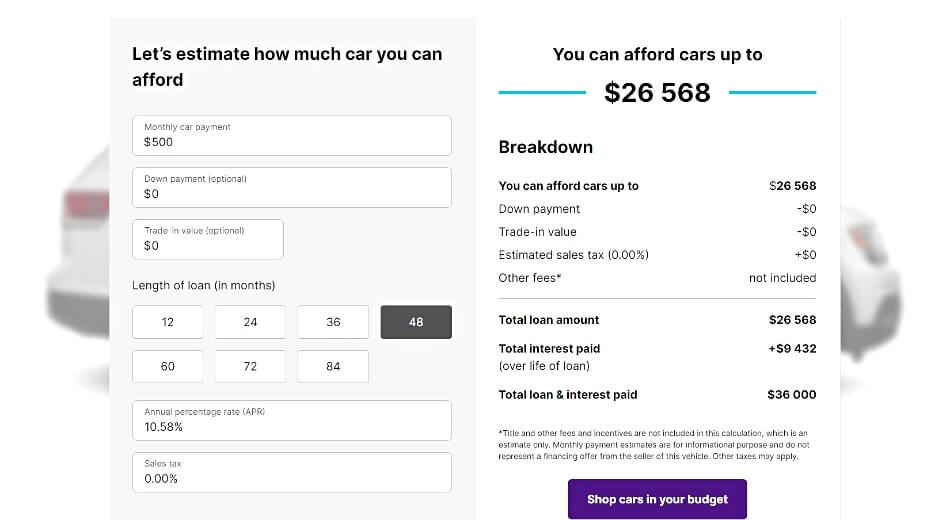

Step 4: Use an affordability calculator to estimate the car purchase price based on available disposable income and downpayment.

Cars.com has a good affordability calculator with downpayment and monthly payment inputs. Plug the numbers in and get an estimate right away. (Cars.com Affordability Calculator)

Step 5: Armed with the knowledge of how much you can afford, approach the car dealership and only shop for cars that are well below the budget available for monthly payments. Don’t even check cars that are more expensive because they may be a source of temptation. Overspending leads to unmanageable debt.

Don’t pay the least down payment, offer more

When buying a new car with bad credit, there will be more hurdles involved. A quick way to convince auto loan lenders to offer better rates is to provide a larger down payment. For instance, if the asking price for a vehicle is $20,000, paying a down payment of $10,000 means that the loan company has to lend half of the money. It brings down the monthly repayments too.

Be cautious about buy-here, pay-here lots

The tactic is mostly implemented by independent dealerships that want to flip used cars and make a quick buck. They even lure customers with catchy adverts such as “No credito, No problema” or down payments as low as $250 or $500.

We take issue with such lenders because they pair customers with a network of third-party lenders. The pool of their in-house financers doesn’t consist of distinguished banks or credit unions. Interest rates are quite high, sometimes as much as 50%. That means that it’s possible to pay more than the vehicle’s value.

Buy-here, pay-here lots may track the vehicle for the loan duration by installing a tracking device. Repossessions, after failed payments, are often quick and costly.

Some lenders are not flexible with their repayment terms. They may only offer biweekly payments even if you wish to pay monthly. Unlike traditional lenders, they don’t have much care for reporting on-time payments to the major credit bureaus. They report somewhere, but it’s usually to smaller companies like Clarify.

Limit the loan shopping window to two week

Why two weeks? Well, when buying a used car with bad credit, it’s vital to avoid things that can harm scores. Some providers may conduct hard checks to prequalify borrowers. Racking up many hard inquiries means losing more points. Scoring algorithms treat multiple inquiries recorded within 14 days as one entry.

Credit Unions like PenFed or Alliant can offer lower rates

Credit unions are, in fact, the third-largest auto loan originators behind banks and capital finance. They have the advantage of offering better rates. While they accept bad credit, they set the minimum credit score for a car loan at 580 or 600.

Get someone to boost the auto loan application

You likely know someone with a good credit score to buy a car. They may be a friend, parent, or relative. Their name will be on the loan application as a cosigner, and the lender only contacts them in the case of a default. Contrary to popular opinion, co-signing may impact credit in the case of a default.

Don’t know anyone who can help? Some websites offer paid co-signing services, but be skeptical of such services as they are often scammy.

Meet other requirements for a car loan

It’s not all about being a prime or super-prime customer. Lenders are most concerned about the customers’ ability to pay.

Many people have bad credit resulting from past credit mistakes or unforeseen situations. On the other hand, they may have high incomes.

Get approved by showing the dealership that you qualify in other aspects. Being a homeowner or having a spouse may even increase the chances of qualifying for auto loans.

Don’t be afraid to explain the cause of negative entries in reports such as collections. The lender may be understanding, but that does not mean that you should lie. Offer genuine reasons that can be substantiated.

Don’t rush

Shopping with a bad credit score for a car loan can often seem impossible. It creates the pressure to take any offer on the table. But take time to evaluate loan agreements, amounts, rates, penalties, etc. Never sign before reading the loan agreement closely.

How to Increase Your Credit Score for a Car Loan?

Good scores translate to lower APRs and lots of savings. The best minimum FICO score for auto loans to aim for is about 661-680. Some viable strategies to try include:

- Add information about recurring bills and rental payments to reports: Some services can help at a fee, including Rent reporters and LevelCredit.

- Check for credit report errors: Order report copies from annualcreditreport.com and check for errors. File disputes personally or consider hiring credit repair companies for a done-for-you approach.

- Reduce utilization rates for credit cards: Avoid accumulating a credit card balance of more than 30% of the available limit. Consider paying down large balances to return the account to a low credit utilization rate.

- Keep old accounts alive: Don’t pay off and close old accounts. They contribute more points than new accounts.

- Apply for credit builder loans or secured cards before the purchase: Build up positive credit points by honoring all monthly obligations for new credit products.

Read More:How to Dispute Credit Report Errors?

Bottom Line

Regardless if a consumer is buying a car with poor credit or bad credit, it’s essential to weigh all loan alternatives. Capital finance or bank loans are not necessarily the cheapest.

The credit score needed for an auto loan will also vary depending on the selected originator. It’s also vital to stick to the affordability limits. High monthly repayments can make it challenging to fuel or service an expensive car.