What is a Fair Credit Score?

Disclaimer: We offer completely free content to our users. However, articles or reviews may contain affiliate links and we may earn a commission. Learn more about how we make money.

If you have a fair credit score, it simply means that your scores are not too bad. On the flip side, they’re not good. They are “merely fine.”

Credit scores are a measure of risk. Fair scores tell lenders that you might be at the risk of defaulting on a loan but not as much as someone with a poor score. Existing in this state of equilibrium is not to be desired. Loan companies reserve their reasonable rates to low-risk individuals. While they may approve your loan application, they can impose stricter restrictions, such as higher-income requirements.

You’ll learn more about what a fair credit score is and the steps to correct this situation. We share how to challenge the three major credit bureaus to remove errors from your reports. It’s a viable strategy to turn fair scores into good scores fast. Let’s get started.

Do I Have a Fair Credit Score?

Yes, you have a fair score if your FICO Score Report Card shows a score that falls into the FICO score range of 580-669. The Fair Isaac Corporation (FICO) is one of the many providers of scoring algorithms used to measure risk based on data in credit reports.

When looking at the VantageScore model, it categorizes fair scores as ranging between 601-660. Lenders can choose the scoring algorithm they use. The models are designed to help them measure the risk of defaults.

The labels attached to various score ranges are very malleable. Different lenders may also have an opinion on what is considered fair credit. Some sources consider FICO scores of 601-660 as fair. Nerdwallet places the fair range as 630- 689.

If the national average credit score is quite high, the fair credit score range may also increase to reflect this. Currently, the national score average is 711 (as of 2020). It’s the highest score ever, so you can consider that lenders will shift their perception of what they consider fair (not good and not bad).

If your scores are fair, you may access various loans, but you’re still considered a subprime borrower. Traditional banks typically don’t extend loans to subprime consumers, a position many institutions had to take following the 2008 financial crisis.

It doesn’t mean that you should not apply for their loan products. Some traditional institutions may be open to accepting fair borrowers with scores of at least 620. They will look at other factors that may show the borrower’s ability to repay the debt, such as high-income or available disposable assets.

| Score range | Rating | Credit score meaning |

| 300 – 580 | Bad | Possible history with bankruptcy

60-day delinquencies High utilization on revolving credit accounts |

| 580- 669 | Fair | Late payments

High CUR Short credit history |

| 670- 739 | Good | No recent delinquencies

No bankruptcies Adequate credit history length |

| 740-799 | Excellent | Long credit history

No bankruptcy Good credit mix Low utilization rate |

| 800 – 850 | Exceptional | About 9 open credit accounts

Very few hard inquires Over 20 years credit history |

Fair Credit vs. Good Credit: Limitations and Opportunities

There’s a lot of motivation for raising a fair credit rating to higher tiers. So, what does fair versus good credit get you?

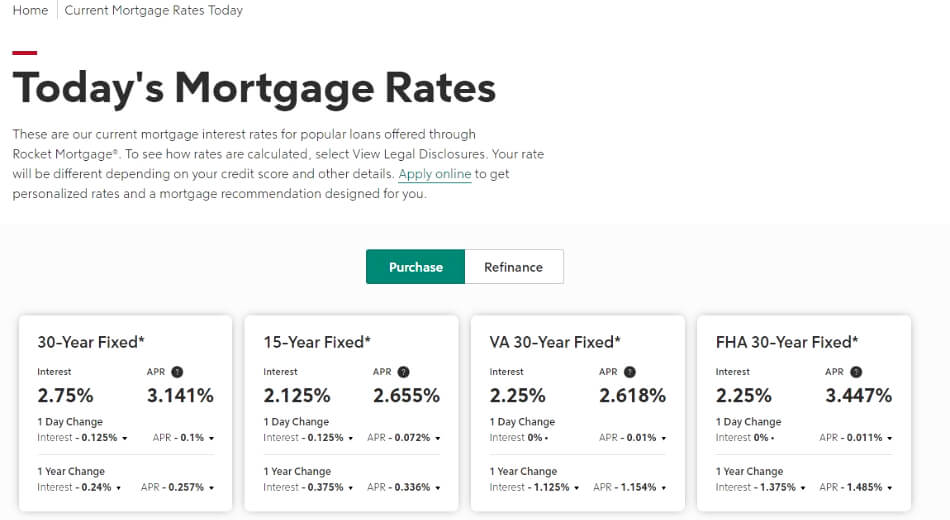

Mortgage Rates

What is a fair credit score for a mortgage? Rocket Mortgage (former Quicken Loans), the largest originator of mortgage loans in 2020, places the lowest score needed to qualify for a conventional mortgage at 620. For FHA-backed loans, the lowest permitted score is 580. For VA-insured loans, the lowest score ranges from 500-550.

Getting approved is one part of the battle. There will be higher rates. That’s because lenders have to account for the added risk of taking on customers with low creditworthiness.

Now, if the rate for people with fair credit is up to 1% higher than the advertised rate, how much more could someone pay compared to someone with good credit. Let’s tackle this question with this handy table.

| With 620 score | With 750 score | |

| Loan amount | $200,000 | $200,000 |

| Interest rate | 3.5% | 2.5% |

| Loan term | 15 years | 15 years |

| Monthly payments | $1,430 | $1,334 |

| Total mortgage cost | $257,358 | $240,044 |

While you may have a fair credit score to buy a house, it may be worthwhile to postpone the purchase in lieu of improving scores as it can significantly affect the mortgage cost. A prime consumer can often borrow more. That positions them to purchase the home of their dreams.

Personal Loans

Bankrate estimates that interest rates for people with excellent credit range from 10.3% to 12.5% on personal unsecured loans. People with fair or bad credit could pay up to 36%. Because personal loans are often unsecured and not backed by any asset, it will be increasingly difficult to qualify for the loan products without higher credit scores.

Most mainstream lenders require a minimum score of 660. When borrowing with fair credit in the private lenders market, some companies may charge APRs in the triple-digit range.

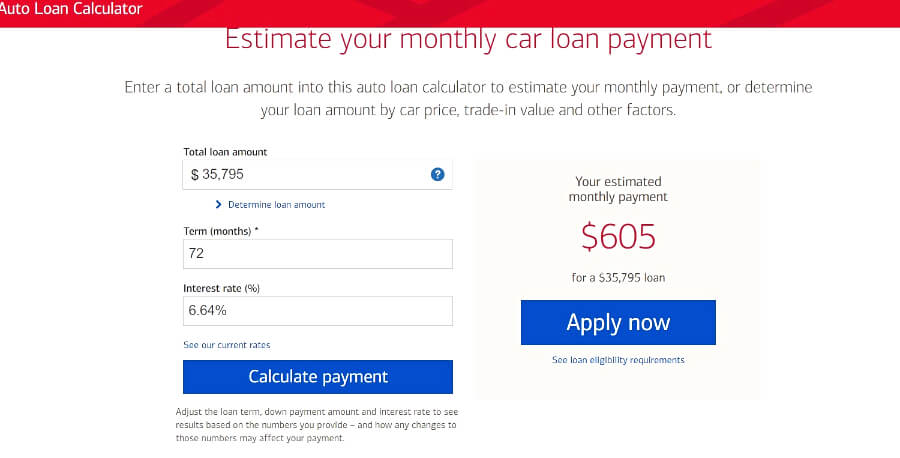

Car Loans

What is a fair credit score to buy a car? You can qualify for a car loan with any score. But subprime consumers often contend with limited options and higher monthly rates.

According to the Experian AutoMarket Insights Q4 2020, near-prime consumers paid a rate of 6.64%, while prime consumers paid 3.69%. The rate for super-prime consumers was 2.65%. The report categorizes people within a score range of 601 – 660 as near-prime, the same range for fair scores.

How does this look in real life? Consider this table that incorporates figures from the 2020 report:

| Near-prime | Prime | |

| Rate | 6.64% | 3.69% |

| Average new vehicle value *2020 | $35,795 | $35,795 |

| Popular loan term | 72 months | 72 months |

| Monthly payment | $604 | $555 |

| Total costs | $43,495 | $39,958 |

Credit Card

Card companies offer various cards targeted at consumers with different scores, including those with bad or fair credit. They may not be the top-rated credit cards, but they come with plenty of credit card offers, such as cashback programs.

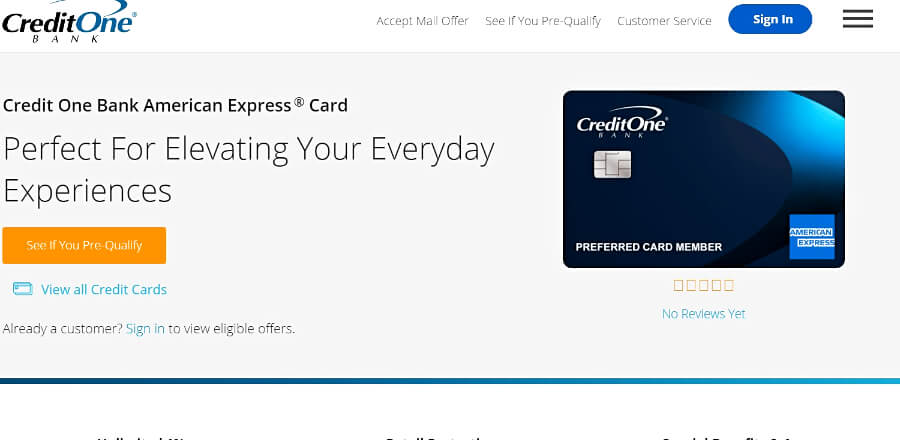

One popular card for fair scores is the Capital One Bank American Express® Card. It has a starting APR of about 23.9% and an annual fee of $39. With not-so-good scores, the APR on many credit cards may be up to 30%. People with poor credit may only access secured credit cards meant to help them rebuild their creditworthiness.

How to Improve a Fair Credit Score?

You have a lot of motivation to get your scores up as the interest rate for fair credit score on most loans is above the average paid by other consumers. There are various strategies to try to improve scores:

1. Disputing mistakes in credit reports

Three of the most common mistakes in credit reports include incorrect account details, missing information, and PII mistakes. For instance, your credit limit on cards may be missing. It may increase your credit utilization rate, which contributes up to 30% of your FICO score. Payment history mistakes such as a wrong delinquent entry may deduct points by up to 100 points.

The Fair Credit Reporting Act entitles every person to an error-free report. You have the power to ask for re-investigations by writing to the credit bureaus. The investigation process takes about 30 days. Original furnishers must verify the information they previously added. By having a major mistake such as a late payment removed, scores may improve substantially.

Many people choose to work with credit repair companies during this process. Lexington Law reports that they have about half a million customers at any given time.

Repair agencies make the process easier by handling all the correspondence with the bureaus. Other top providers in this field include The Credit People, Creditrepair.com, and Ovation.

2. Adding new trade lines to reports

All the major bureaus allow customers to add information about their bill payments to their credit reports. For instance, through the Experian Boost program, Experian even allows clients to add their internet streaming subscriptions.

Another way to add information showcasing positive credit use is by finding someone to add you as an authorized user to their card. There will be no need to use the card for purchases. As long as the account owner makes the repayments, their positive history also reflects in your reports. It may be as fast as next month.

3. Signing up for credit rebuilding products

Consider signing up for secured personal loans offered by banks and online lenders. It’s possible to use assets that have monetary value as collateral or a cash deposit. The creditor will report your history of repayments to the bureaus, building up your credit.

Another class of credit building products is secured cards offered by the major card companies. You will need to make an initial deposit, which determines your limit. After establishing a good track record of paying down balances, the card company may raise the card limit without requiring another deposit.

4. Having a financial backup plan

How is having a backup plan going to move you from a fair to good credit score? Well, it ensures that you can still keep paying down your debts in case you lose your job or incur a life-altering emergency. You need to have at least three months of your regular expenses saved up. Currently, only 39% of Americans can pay for a $1,000 emergency without using credit.

Read More:How Long Does It Take to Repair Credit?

Conclusion

You have learned what is considered a fair credit score. It starts at 580 and is below 700 points. Falling into this score range may come with challenges such as obtaining affordable credit products. Fortunately, there are various ways to move into a better rating by utilizing credit rebuilding products or disputing report errors.