No explicit communication on when to stop subscribing

No service guarantee

Currently, involved in a consumer protection lawsuit

Disclaimer: We offer completely free content to our users. However, articles or reviews may contain affiliate links and we may earn a commission. Learn more about how we make money.

Searching for the latest Lexington Law reviews? For nearly two decades, clients have trusted Lexington Law for credit help. They challenge the CRBs to remove inaccurate items from their clients’ reports.

They have moved from the slower mail-based dispute filing to a faster process made possible by digital partnerships. Their main strength is that they leverage the law to help clients meet their credit goals. Few credit repair companies have a lawyer-based process.

Planning to sign up? Consider the following Lexington Law results:

The firm has sent over 183 million challenges and disputes since 2004;

Over 1.5 million negative items were removed from their clients’ reports in 2019;

Clients have had over 56 million removals of inaccurate items since the start.

Lexington Law reviews from previous customers paint a picture of a dedicated and caring company. They go above and beyond their mandate by also offering excellent advice. Lexington Law has developed help resources and offers debt & budgeting tools.

There’s a lot more to learn in this Lexington review 2021. See all the reasons to become part of their 500,000 active clients. We will also cover some of the limitations of their platforms for a complete picture.

Lexington Law is not an online credit repair company. It’s a general customer advocacy law firm. All credit repair services are under the helm of John C. Heath, Attorney at Law, assisted by about 24 attorneys and 400 paralegals/agents. He took charge as the Director Attorney in 2004, ushering a new era centered on credit repair services.

In 2010, the firm hit a major milestone by garnering over 1 million sign-ups since its start. They operate from two main locations. Cody Johnson, Managing Attorney, heads their Phoenix Arizona office. John C. Heath oversees operations at their Utah office, with help from Cynthia Thaxton, Assistant Managing Attorney.

The firm is part of Progrexion’s family of credit consumer brands, along with creditrepair.com and credit.com. Working with Progrexion affords Lexington Law access to the patented technology that drives the dispute process. The unique selling proposition is that they offer a lawyer-driven process. The firm states that they use every legal angle in an attempt to repair credit.

Some of their practices have gotten them in trouble in the past. CBE Group and RGS Financial — which are large collection agencies — had sued the company over allegations of fraud for sending large volumes of letters to dispute claims. Initially, the plaintiffs received a $2.5 million settlement against Lexington Law and Progrexion. But in 2020, a judge overturned the verdict.

They are currently involved in a case brought by the CFPB against companies operating under PGX Holdings, including creditrepair.com. It cited that they participated in bait advertising, requesting upfront payments for services, and violating telemarketing rules. Lexington Law has since filed to have the case dismissed.

Now that you’re learning about the lawsuit, should you be worried about the quality of their services? It has not impacted the quality of the services and final results. The suit questions the marketing practices used in customer acquisition by PGX Holdings and affiliated parties.

How Does Lexington Law Work?

The Fair Credit Reporting Act (FCRA) passed in 1970 stipulates that information in customer credit reports should be accurate and fair. It’s essential to make sure that the information is up-to-date, complete, and accurate before applying for credit products or even a job. Customers may open disputes to have any inaccurate information changed by writing to Credit Reporting Bureaus. If they can’t prove that the information is correct, they have to remove it.

Lexington Law leverages this process to fix their clients’ credit. Their four-step process entails:

Step 1: Helping clients obtain copies of their credit reports and analyzing them for inaccurate entries to dispute.

Step 2: Disputing negative items by sending the required correspondence on behalf of the clients.

Step 3: Escalation of disputes for challenges that require additional evidence.

Step 4: Reporting on credit score changes and providing credit counseling tips.

When conducting a Lexington Law firm review, you will also note that they offer a number of extra services. The company can assist in writing:

Goodwill intervention letters – Asking for Goodwill removals entails requesting creditors to remove legitimate negative entries, but it does not have a high chance of success.

Debt validation letters – They are useful when the debt amount is in question.

Cease and desist letters – They inform debt collectors to stop sending communications.

Credit repair is not suitable for people with high debt levels and persons who are struggling to cater to their monthly bills. They should consider other services such as debt consolidation and repayment plans as a means to improve their credit.

As one of the most popular credit repair firms, Lexington Law manages various aspects of its service well. The obvious pros include an ultra-modern platform, extensive market experience, and quality credit educational resources. Additional benefits of the platform include:

Lawyer-driven disputes and escalations: It’s one of the unique features that has helped the firm stand out.

Robust credit monitoring and inquiry assist tools: The firm uses innovative and optimized technologies for faster and higher removals. They report that an average customer will see an average of 8.6 removals by the third month.

Proven results: We like that the firm is upfront with its statistics. They don’t just taunt the benefits of their credit repair process without quoting figures.

Resolved Lexington Law complaints: The company has accumulated about 640 complaints within the last three years on their BBB.org page. They go out of their way to resolve each complaint. That shows their dedication to offering quality services.

Plenty of positive reviews of Lexington Law: As a leading repair firm, Lexington Law has accumulated plenty of feedback that new customers can use to verify the credibility of their service. The company has been featured by top financial sites, adding to its credibility.

Lexington Law has fewer cons than its pros. They are certain things the company can improve on, including:

Wavering reputation: Lexington Law and PGX Holdings have been the subject of subsequent lawsuits, and this has chipped away at their immaculate image.

Lack of a service guarantee: Clients don’t get concrete assurances of removals. They are not entitled to refunds should the company fail to live up to its mandate.

Not highly personalized: In Lexington Law client reviews, we have found past clients thanking the paralegals for answering their credit repair questions. But we still feel that Lexington Law could have a more personalized service where multiple experts help customers in the repair and rebuilding process. Some platforms take the extra step and assign personal managers to each client and offer expert-led analysis.

Positive things clients have said about Lexington Law

We took a look at Lexington Law reviews from users of their Android app. The ratings are mostly 4 & 5 stars.

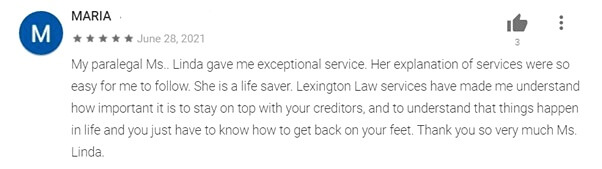

Many people expressed that they like working with their paralegals and speaking to them on the phone. Some even mentioned the paralegals that were helping them by name.

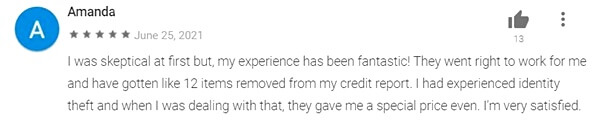

People who had inaccurate entries removed also stated the number of removals they had. A user who had problems with identity theft revealed that she received a special price.

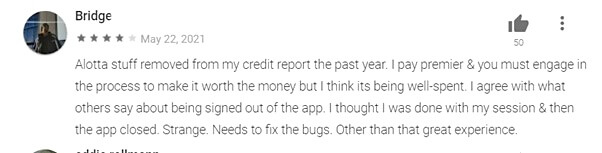

In another Lexington Law review, the reviewer expressed that his money was well spent but pointed out that the app had some bugs as it closed unexpectedly.

Don’t take our word for it. Access more Lexington Law credit repair reviews by real clients from their Apple Store preview page and Trustpilot.

How Does Lexington Law Handle Complaints?

By merely providing any service, a company will have satisfied and unsatisfied customers. Across the board, the best credit repair companies usually receive complaints about their service. After sending the first disputes, CRBs can take anywhere from 30 to 45 days to respond. Customers tend to be unsatisfied when they don’t see results quickly.

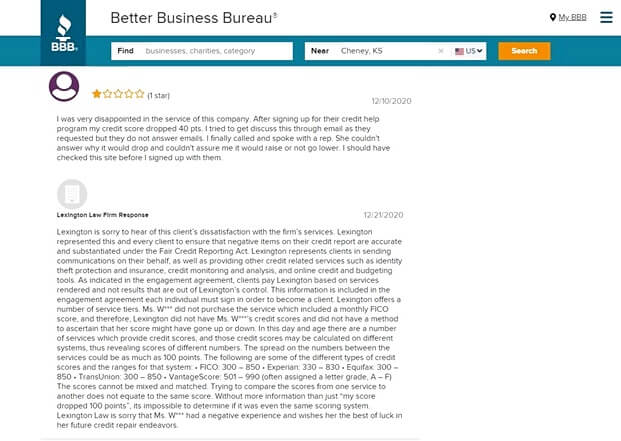

We gauge how credit repair companies handle complaints. How has Lexington Law performed? On the Lexington Law BBB page, we have found that while the firm responds to all complaints, their responses are a bit too formal, with statements such as “Lexington is sorry to hear of this client’s dissatisfaction.”

In some instances, they chose to issue refunds. It’s also worth noting that the firm still charges a fee after canceling any package for services rendered during the month. The Lexington Law ratings on BBB are low at 2.11/5, and they are not accredited.

During your Lexington Law credit repair review, you will no doubt come across other negative complaints. It doesn’t mean that their services are not good. People are more likely to leave a negative review if they are not satisfied than a positive review if they were happy with the service.

If attempts to resolve an issue with the company fail, it’s possible to report to the Consumer Financial Protection Bureau or leave the complaint on their BBB.org page.

How Much Does Lexington Law Cost?

There are three Lexington Law plans. They’re not listed directly on the website. You have to begin the signup process by filling out the form asking for details such as email and names. Now we don’t like this because after abandoning the process, they still send promotional emails.

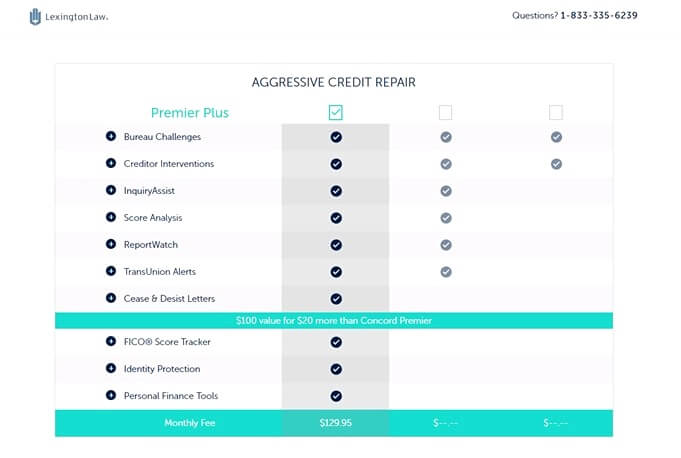

PremierPlus

For $129.95, the Advanced package includes:

Bureau challenges – Identifying and seeking the removal of inaccurate records;

Creditor interventions – Challenging creditors directly to remove non-factual information;

InquiryAssist — Helping clients challenge hard inquiries;

Score analysis — A detailed and comprehensive breakdown of credit reports;

ReportWatch — Personalized coaching on credit report issues;

TransUnion alerts — Daily report tracking on TransUnion;

Cease and desist letters — Sent to overbearing creditors that overstep their bounds.

The package also includes FICO Score Tracker, ID protection, and personal finance management tools.

By paying this Lexington Law cost, the company promises aggressive repair services. It may seem a bit high, but it’s within the industry rates on the top packages offered by other repair firms.

Concord Premier Package

At $20 less, the Concord Premier package doesn’t include the FICO tracker, ID protection, or personal finance management tools. They have also removed cease & desist letters.

Are these features necessary? Well, the letters just tell the creditor to halt any communication about a pending debt. The only limitation of this package is that at $100, we feel that the Lexington Law firm should have also included score tracking. So, it’s not the best value, as it necessitates paying for third-party score tracking.

How will you monitor the progress? The package includes a report watch and TransUnion alerts. It’s possible to see if the nonfactual information has been removed, as it includes daily updates.

Concord Standard Package

The lowest package is the Concord Standard that goes for $89.95. It only includes credit challenges and creditor interventions. A lot is missing from this package, including the ability to have hard pulls challenged. It doesn’t include score or report alerts, which may necessitate signing up to another third-party monitoring service.

Note that the firm charges a first work fee that corresponds to each monthly package price. For instance, the setup cost for the Concord Standard is $89.95. According to the Credit Repair Organisations Act, a company is not permitted to charge any fees upfront or demand advanced payment.

Alternatives to Lexington Law

Lexington Law is certainly one of the most recognized names in credit repair. But they are not perfect! Their service certainly lacks some features that could be found elsewhere.

Companies like Lexington Law offer similar services at the same price points. They also provide extras like Goodwill interventions. Our shortlisted companies have been in the repair industry for a long time. There are independent reviews from past customers that may be used to gauge the credibility of the services mentioned below.

If you’re weighing possible alternatives to Lexington Law, here are the top companies to start looking at:

Sky Blue vs. Lexington Law

Sky Blue may not have the most advanced credit repair platform. To make up for the lack of features, they attempt to offer more value. Their apparent advantage is that clients work with professionals to identify dispute candidates. Each dispute is customized and tailored to each situation.

They also offer additional credit guidance through score assistance and credit rebuilding advice, such as recommending credit repair loans. There is only one package at $79 per month with a corresponding initial work fee. It means paying about $158 for the first month of service.

Lexington Law prices are higher. Even on the cheapest package at $89.95, customers will pay about $179 for the first month. On the positive side, the firm offers a lawyer-driven process, but this may not translate into more removals as the firms use similar dispute processes.

It’s also worth noting that Sky Blue does not have FICO score reporting. Customers will need to sign up with a third party to track their changing FICO scores.

Lexington Law, on the other hand, offers robust score and report tracking tools. Customers receive TransUnion alerts as well as FICO score updates. The PremierPlus package also comes with identity protection and monitoring tools. Working with Sky Blue may mean paying for this extra convenience separately, at a fee between $20- $30.

Sky Blue

Lexington Law

Credit repair experience

32 yrs (1989)

17 yrs (2004)

Guarantee

90-day Money-back

Not offered

Pricing range

Single package $79

$89.85 — $129.95

Initial work fee

$79

$89 — $129

Services

Challenges

Score analysis & monitoring

Creditor interventions

Credit rebuilding guidance

SOL Research

Challenges

Score Analysis

Inquiry target

TransUnion monitoring

FICO Analysis

Creditor Interventions

Personal finance manager tools

Identity protection & insurance

Credit score coaching

Mobile Applications

Not Available

iOS & Android

Credit Saint vs. Lexington Law

Right out of the gate, Credit Saint leads with their Money-back 90-day guarantee. It means that customers will have a more worry-free service. Both companies have similar years of experience.

But Lexington Law regains their hold with comparatively cheaper first work fees. The company shows its technological prominence with more tools, including a personal finance manager.

The Clean Slate package from Credit Saint at $119.99 is just $10 cheaper compared to Lexington Law’s Premier Plus. But the initial work fee is $65 more expensive. An average customer stays with a credit repair company for 6 months. So, the plans typically go for the same price, and there are no savings to be made by choosing between them.

Creditrepair.com and Lexington Law are Progrexion consumer brands. They use similar technologies to provide credit repair services to their customers. Clients with a keen eye will notice many similarities between their platforms. But they have some differences.

Lexington Law leverages its strategic legal advantage by offering a lawyer-driven process. Its packages cost more. Their website even appears more intuitive and easier to navigate. But some of the content is similar such as the FAQ section.

Mobile apps provide similar functionality that includes FICO score monitoring, Transunion report watch, and case tracking. Choosing between the two will boil down to a matter of preference. In addition, Lexington Law boasts of a much stronger brand. Creditrepair.com provides more for less.

CreditRepair.com

Lexington Law

Credit repair experience

9 yrs (2012)

17 yrs (2004)

Guarantee

Not offered

Not offered

Pricing range

$69.95 — $119.95

$89.85 — $129.95

Initial work fee

$69.95 — $119.95

$89 — $129

Services

Challenges

Score Analysis

TransUnion monitoring

FICO Analysis

Creditor Interventions

Personal finance manager tools

Identity protection & insurance

Challenges

Score Analysis

Inquiry target

TransUnion monitoring

FICO Analysis

Creditor Interventions

Personal finance manager tools

Identity protection & insurance

Credit score coaching

Mobile Applications

iOS & Android

iOS & Android

Is Lexington Law Worth It?

From our analysis, Lexington Law is a legitimate credit repair company worth the money. They have proven results from helping thousands of clients. Their credit repair app is one of the most downloaded and highly rated.

Clients can even read Lexington Law testimonials on their app pages or TrustPilot. We still acknowledge that there is a lot the company can do to improve its services, including providing a guarantee and solving complaints more amicably.

So, does Lexington Law really work? Yes, it does. Even if there have been negative things said about the company, it’s worth registering as a new client or signing up for the initial call that can help gauge the suitability of their service. During the call, they review reports and current scores. Their smartphone apps are also free to download.

Lexington Law has had the privilege of serving more than one million customers. We like their robust packages that feature a variety of credit monitoring and repair services. The only aspect of the service that we don’t like is that they don’t offer a service guarantee and are not quick to issue refunds to unsatisfied customers.

Lexington Law cannot legitimately challenge accurately reported items and have them removed. They may remove charge-offs or remove late payments if they were inaccurately or unfairly reported.

Any firm that states that they can remove judgments regardless if they were accurately reported may be out to scam its clients.

There is no stated timeline as each case tends to be unique. However, the firm must begin work on the client’s credit before collecting the initial work fee billed after five days. CRBs may take anywhere from 30 to 45 days to respond, and this determines when you start seeing improvements.

The company offers three plans at $129.95, $109.95, and $89.85. They recommend that customers should choose the advanced aggressive package for the best results. There will be an initial setup fee to be paid for each plan, and it ranges from $89 – $129. For instance, by signing up for the PremierPlus package, the first month’s bill would amount to $258.95.

The number to call is 1-877-381-5088. Service hours are from Monday – Friday, 7 a.m. – 7 p.m. MST. They don’t serve customers in Oregon and North Carolina.

Navigate to the main website or download the app to sign up for their services. They provide a number to call if you require a free consultation. It may be useful if you’re not certain about having errors in reports or how the process works.

Yes, they can get rid of charge-offs only if they have been wrongly reported and don’t belong in the credit report in the first place. They can’t have legitimate items deleted, either by contacting the credit bureaus or past creditors directly.

The company is not BBB accredited, but they respond to client complaints on the platform. There are reviews on Lexington Law on BBB.org, along with a rating that has been automatically generated. The rating is not entirely based on customer ratings.

Share this article!

Gerald Dunigan

Gerald is the founder and editor-in-chief of CreditFixed.com. Over 13 years of experience in credit repair companies and finance. Each text is published after its detailed proofreading